Introduction

Mobile banking has crossed the threshold from a convenient channel into the primary interface through which most people manage their financial lives. According to SQ Magazine, there are over 2.17 billion mobile banking users worldwide as of 2025, with Europe reaching 76% penetration and Nordic countries exceeding 87%.

The question for 2026 is no longer whether to invest in mobile banking capabilities, but which layer of the stack will define the next generation of user experience. The answer, increasingly, is transaction data.

This article maps the most significant trends in mobile banking this year.

Transaction data standardisation

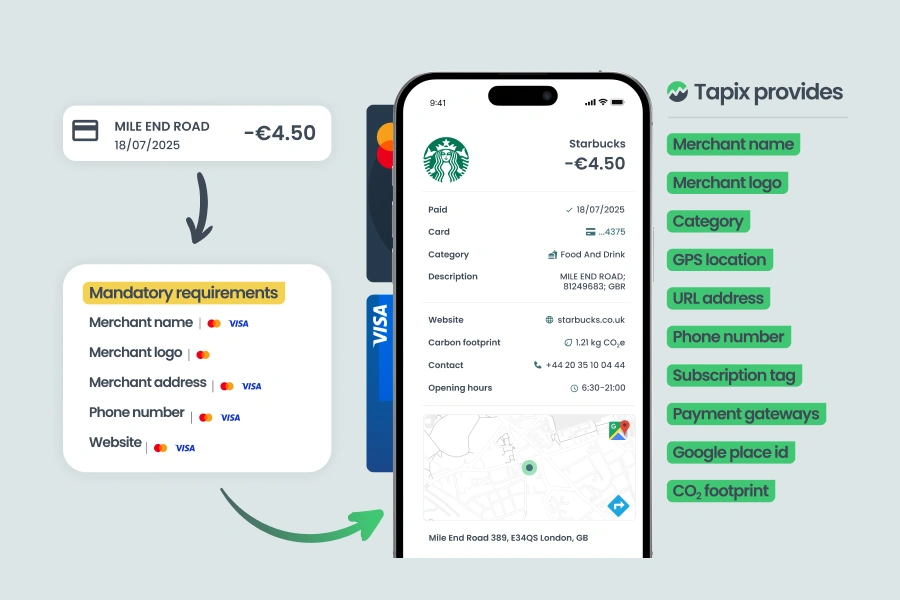

The most consequential change of the year is a regulatory one. Mastercard’s AN4569 mandate is already live, requiring acquirers and issuers to pass through clean merchant names, accurate locations, and structured transaction descriptors. Visa’s equivalent enhanced merchant data mandate is following closely, extending requirements to include merchant website URLs, contact information, and enriched category data.

Want to know more? Read about Visa/Mastercard Mandate Compliance.

This matters because the raw transaction descriptions have been one of the most persistent failure points in digital banking UX. Real-world implementations show the impact clearly. Swisscard, one of Switzerland’s leading card issuers, resolved the mandate in partnership with Tapix, bringing clean merchant data to cardholders across its portfolio. The project also ties into a broader memorandum on multibanking in Switzerland, where enriched transaction data plays a critical role in enabling seamless account aggregation and cross-bank financial visibility.

Beyond Mastercard and Visa, PSD3, FIDA (Financial Data Access), and CCD2 (Consumer Credit Directive) are all pushing banks and fintechs toward richer data sharing and higher data quality standards. For enrichment providers like Tapix, this mandate era is the clearest proof yet that what was once considered a “nice to have” - accurate merchant names, logos, GPS location, payment gateway identification, and contact details - is now the mandatory baseline on which every downstream banking feature depends.

The subscription economy under control

The scale of the recurring payments challenge is larger than most banks realise. Tapix data shows that the average person makes around 24 transactions per month, of which 5 are recurring payments - and industry estimates place the share of recurring payments across all card and bank transactions at between 15% and 50%, depending on the customer segment and market. On fintech apps, where users consolidate subscriptions and direct debits, up to 50% of all transactions are recurring in nature. This is the foundation of everyday financial life.

The strategic implication is straightforward: who owns recurring payments owns primary bank status. A bank that gives customers a single, consolidated view of every subscription, direct debit, and instalment - with the ability to block, pause, or cancel directly from the app - becomes the default account where financial life is managed.

As such, the most forward-thinking banks are moving beyond simple recurring payment detection to a full Recurring Payments Intelligence layer.

Real-time UX is the new gold standard

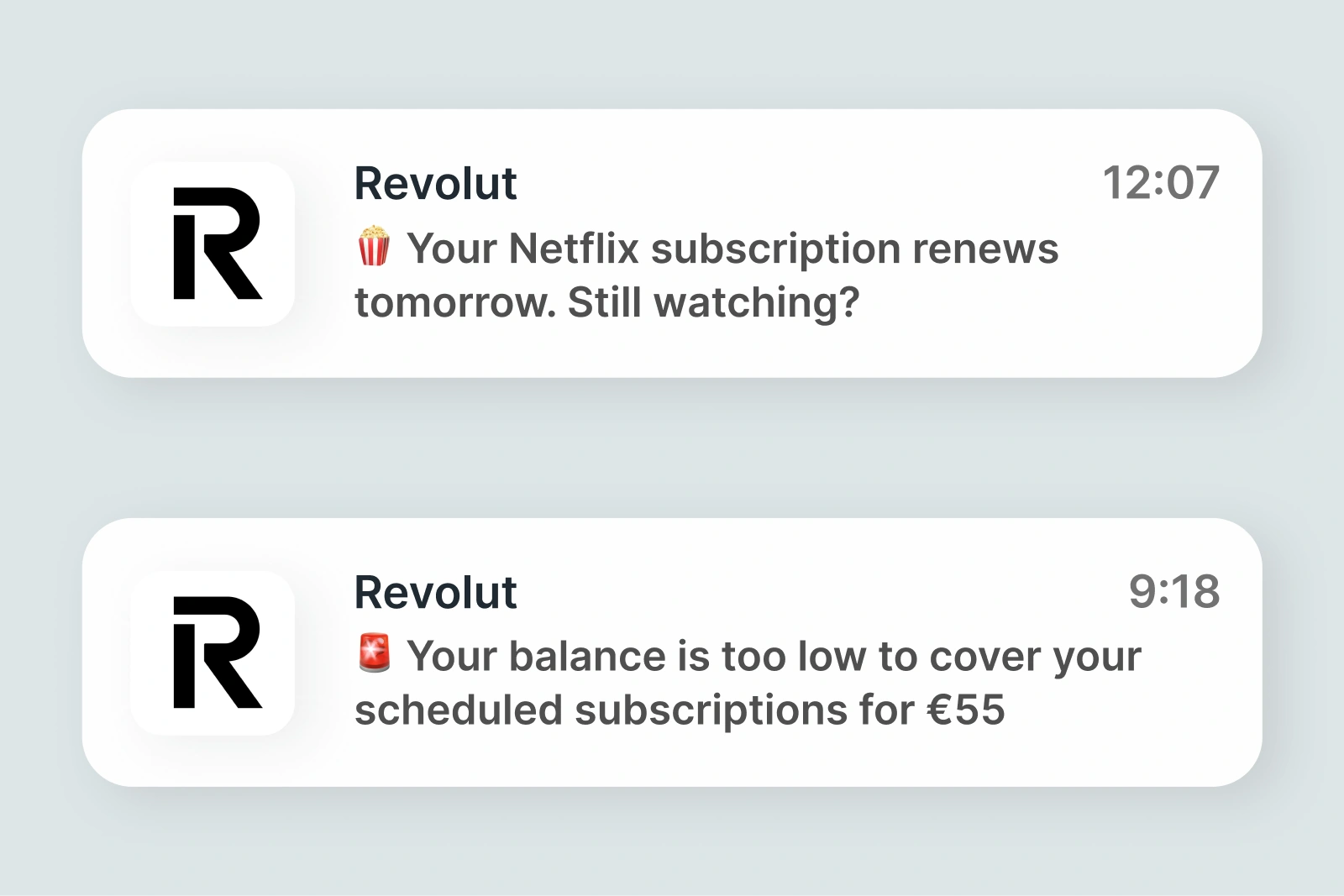

Speed is part of the product. Delays break trust, so expectation is now instant: push notifications the moment a payment is made, categorisation that appears before the user closes the app, and live balances that reflect every transaction without page refresh.

The future of digital banking UX has deep implications for transaction enrichment. It can no longer happen in a nightly batch job. Banks are increasingly demanding real-time or near-real-time enrichment APIs, where the merchant’s name, logo, category, and contextual tags are appended to a transaction within milliseconds of authorisation. The enrichment layer is now part of the payment flow itself.

When a user receives an instant, accurate, categorised notification - “You spent €24.50 at Starbucks (Coffee & Drinks)” - immediately after tapping their card, they perceive their bank as intelligent and trustworthy.

PFM evolving into action-driven financial coaching

Personal Finance Management tools have been a staple of digital banking since the early 2010s. But the static dashboard model is being replaced by something fundamentally more useful: proactive, action-driven financial guidance.

The best example is BBVA’s Financial Coach, which moves customers from passive awareness to active progress through a structured coaching loop. The system starts with a diagnostic of income, spending, savings, and loan repayments, then translates this into concrete goals the user can choose to pursue - building an emergency buffer, reducing a specific expense category, or freeing up cash flow. Step-by-step guidance evolves with their behaviour over time.

This approach treats money management like fitness - not a single moment of advice, but an ongoing process that builds capability and confidence over time. To power this kind of coaching, the underlying transaction data must be flawlessly categorised, consistently structured, and rich enough to identify behavioural patterns over time.

The shift from “what happened” to “what should I do next” is defining the new personal finance management trends.

AI becomes the primary interface layer

AI banking trends are one of the main topics for 2026. While we had simple chatbots and assistants for quite a while, more complex AI tools are slowly becoming an integral part of modern finances.

Leading European fintechs are already there. bunq has introduced a conversational “ask your finances” layer that allows users to query their own data in natural language. BBVA’s Financial Coach replaces static menu-driven flows with a guided intelligence system. Revolut is deploying early copilots and contextual insights that surface proactively. Nubank’s dashboard grounds recommendations in nuFormer, a proprietary foundation model trained on large-scale behavioural and transactional sequences.

Want to know more? Read why chatbots rely on high quality data.

The result? Navigation becomes query-based interaction. Dashboards become answers and actions. The UI is now an interpretation of your data. And that means your data needs to be searchable, structured, and semantically rich.

This is where transaction enrichment becomes the invisible infrastructure of AI banking. An AI that cannot distinguish between a subscription payment and a one-off purchase, or between a pharmacy and a general retailer, cannot give meaningful financial guidance.

Better Security Features

As with AI advancements, security features are becoming more robust following the mobile industry privacy trends, offering biometric protection, extensive authorisation and other protective measures. However, these can be further improved with more accurate transaction data and AI integration:

- Advanced Biometric Authentication: Using voice recognition or advanced facial recognition for additional security layers.

- Real-Time Fraud Alerts: Instant alerts for suspicious activities, with the ability to freeze accounts immediately.

- Enhanced Privacy Controls: Giving users more control over their data, such as deciding what information third parties can access.

Mobile banking apps are also adopting new innovations to safeguard user information while ensuring compliance with global regulations like GDPR and PSD2. We are talking decentralized or blockchain-based storage solutions, end-to-end encryption enhancements or more transparent data policies that allow customers to control, restrict, and delete their personal information in compliance with GDPR and other privacy regulations.

Discover the next big mobile banking trends at the Top 135+ Must-Attend Fintech Conferences.

Progressive disclosure UX

Banking apps have historically competed on features by adding them. The result, in many cases, is interface overload: tabs, cards, and notifications competing for attention, leaving users overwhelmed and unable to find what they actually need.

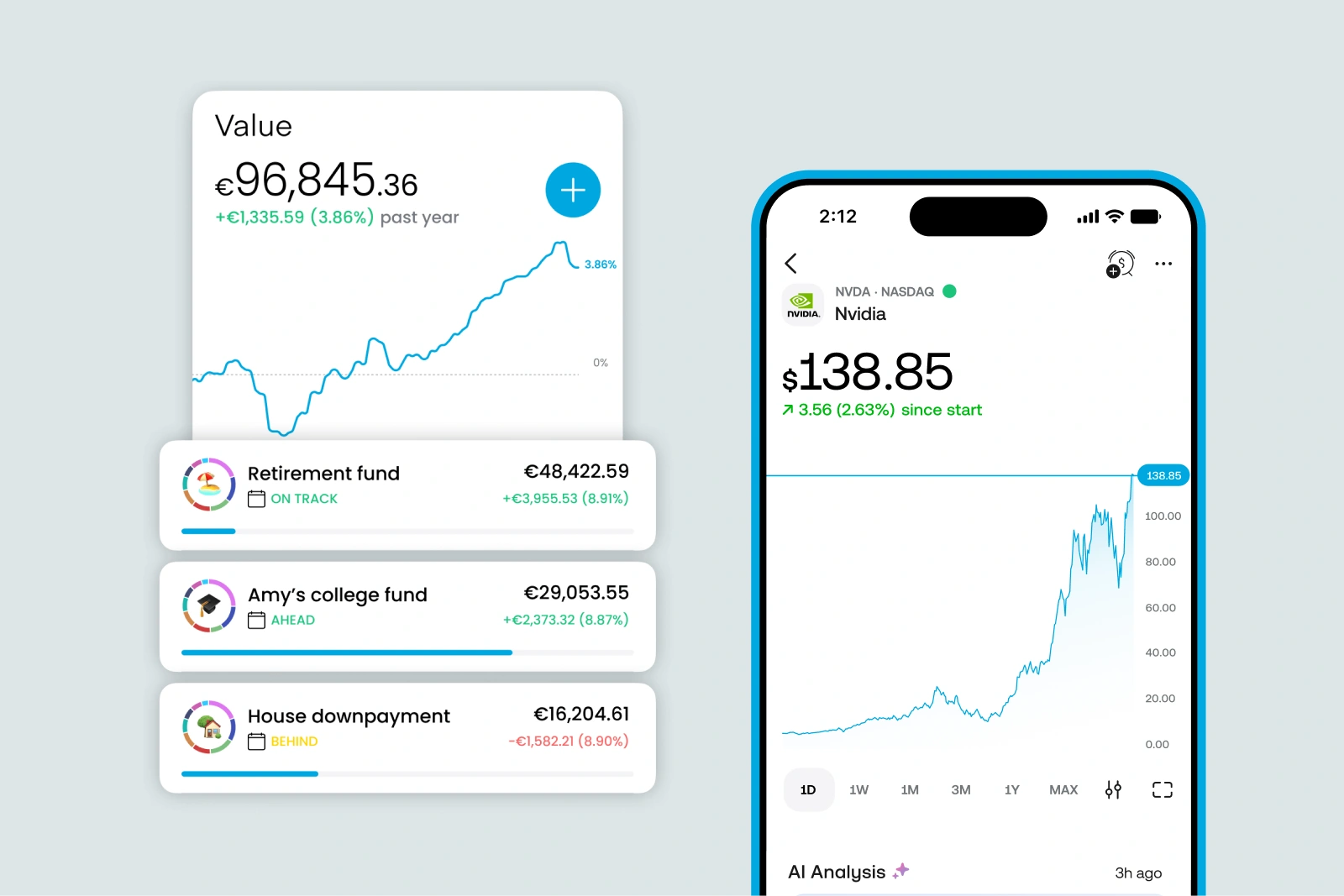

This year's design philosophy, exemplified by Trading 212 investment platform example, runs in the opposite direction. The principle is progressive disclosure: present the essential information first, clean and simple (portfolio snapshot). Make depth available, but only on the user’s terms (individual holdings).

Many banks still hide transactions behind many clicks, but banking is finally catching up to the right pattern. The transaction list is the most obvious application: a clean merchant name, logo, and category tag at the top level; full enrichment detail (GPS location, website, contact, recurring status, CO2 tag) available one tap deeper. Revolut is a good example of this, showing all the important information in one unified, customisable dashboard.

Banking as lifestyle OS

The most ambitious vision in digital banking is the idea of the banking app as a lifestyle operating system - a contextual layer that adapts to what you are doing, not just what you have spent. Banks are expanding well beyond financial transactions into adjacent life domains:

- Travel: integrated travel insurance, FX conversion, eSIM access, airport lounge management

- Deals and rewards: card-linked offers personalised to actual spending behaviour

- Sustainability: carbon footprint insights per transaction, Eco tips, green product suggestions

- Subscriptions: full recurring payments overview with control and prediction

- Life event budgeting: spending plans tied to real-world moments like moving house, having a child, or starting a business

The bottom line of this trend is that transaction data becomes the product layer. The next step is contextual interface development where the app home screen switches dynamically based on where you are or what life event you are navigating. You land at an airport, and the dashboard shifts to travel mode. You just got paid, and it surfaces savings suggestions. You haven’t paid a bill in a while, and it flags it proactively.

Top mobile banking features of 2026

Consumer demand for specific banking app features has continued to specify around a consistent set of priorities. Community research and user surveys consistently surface the following as the most requested improvements:

- Automatic recurring payments management: the ability to see all subscriptions in one place, track changes, and cancel with one tap

- Proper transaction categorisation: readable merchant names and accurate spending categories that reflect real-life behaviour

- Running balance column: a live, always-accurate view of available funds across all accounts

- Instant purchase alerts: real-time, enriched notifications at the moment of payment

- Proactive financial guidance: not just spending history, but forward-looking coaching and suggestions

- Rewards tracking: visibility into what rewards and cashback have been earned from each transaction

- Granular notification controls: choosing exactly which alerts to receive and how

- Digital account opening: creating and managing accounts entirely within the app environment

- Zero balance payments: the ability to fully pay off a credit balance in a single tap

In 2026, the question is no longer whether to enrich transaction data. The mandates have answered that. The question is how far ahead to build - and whether your enrichment layer is fast enough, accurate enough, and rich enough to power the banking experience your users expect next year, not just the one they tolerate today.